Image credit: TheStreet

A mortgage is an important financial commitment that homeowners make and the payment is often the most expensive in the household budget. From time to time people may suffer from financial stress and be tempted to skip a mortgage payment to make ends meet.

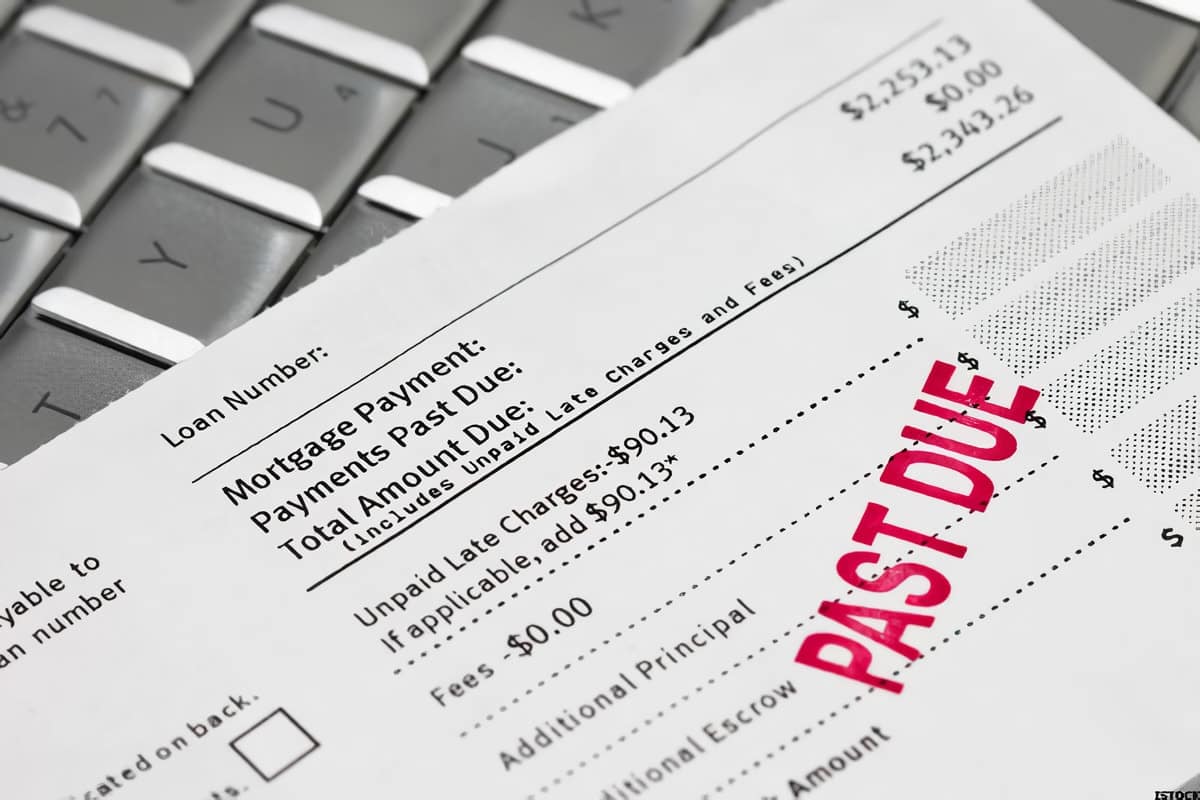

Below is valuable information on why it is imperative to keep your mortgage payments consistent and the consequences if they are missed.

Communicate With The Lender

As with most things in life, communication is important. If a homeowner is struggling to find the means to make their mortgage payment, reaching out to the lender should be one of their first tactics to overcome the situation.

Lenders don’t want homeowners to default on loans, as it affects both parties in a negative way. They will often work with homeowners on ways to resolve the situation even if it means re-evaluating the loan terms.

How Late is the Payment?

Short-Term – Mortgage payments like credit cards usually have grace periods which offer a short span of time (ex. 10-15 days) after the mortgage due date where lenders will accept a mortgage payment without a late penalty. You can find your grace period time frame in your loan terms or by contacting your lender.

1 Month – Missing your mortgage payment by a month is when lenders will generally make a phone call or write a letter to the homeowner stating the missed payment. There will probably be a late penalty fee of some sort. This is also the time period that lenders will report missed payments to creditors.

Multiple Months – Once a mortgage payment is missed by 2 months the collections process with lenders becomes amped up and homeowners are considered in default of the loan. Depending on the lender, 3-4 months is when foreclosure begins to become an option. As mentioned above, during these months communication with the lender is the best step to remedying the situation without having to resort to a more serious consequence.

How Will Credit Scores be Affected by Missed Mortgage Payments?

As mentioned earlier lenders typically report missed payments every month. So if a homeowner falls late on their payment during the short-term grace period, that will not be noted on the credit report but anything after a month will. Several factors go into determining just how much a credit score will be affected by a missed payment. How often a homeowner has been late on payments and how long they have been late are examples of some of those factors. After receiving a drop on a credit score it takes some time to boost it back up to the number it once was.

What Can Homeowners Do If They Cannot Afford Their Homes?

If after discussing their situation with lenders, homeowners still cannot find a way to make their mortgage payments affordable, one option is to sell the home. Granted this will depend on the market conditions and how much the homeowner will actually make upon selling their home. The goal would be to sell the home to make enough money to pay off the mortgage in its entirety.

The next and more serious option as it affects a person’s credit score for many years would be to claim bankruptcy. This is a worst-case scenario and should only be discussed when all possible options have been exhausted.